- CoolByMichael

- Posts

- The Credit Score Chronicals

The Credit Score Chronicals

Plus a step by step guide on how to save thousands.

Michael Cool

January 07, 2025

The Credit Score Chronicles: Your Financial Report Card (But Way More Important) 🎓💳

Are you sitting in your room, wondering why everyone keeps talking about credit scores like they're the new viral TikTok dance? Well, grab your caffeinated beverage of choice, because this newsletter is about to spill the tea on that mysterious three-digit number that has more influence over your future than your search history.

Why Your Credit Score Hits Different

Let's cut through the BS - your credit score matters more than the number of followers you have on Instagram (shocking, I know). Picture this: You've finally graduated, ready to lease that sweet apartment downtown where you can actually have a bathroom to yourself. But plot twist – your credit score is giving "needs improvement" energy, and now you're stuck with four roommates in a place where the kitchen doubles as someone's bedroom.

Here's some data that'll make you choke on your ramen:

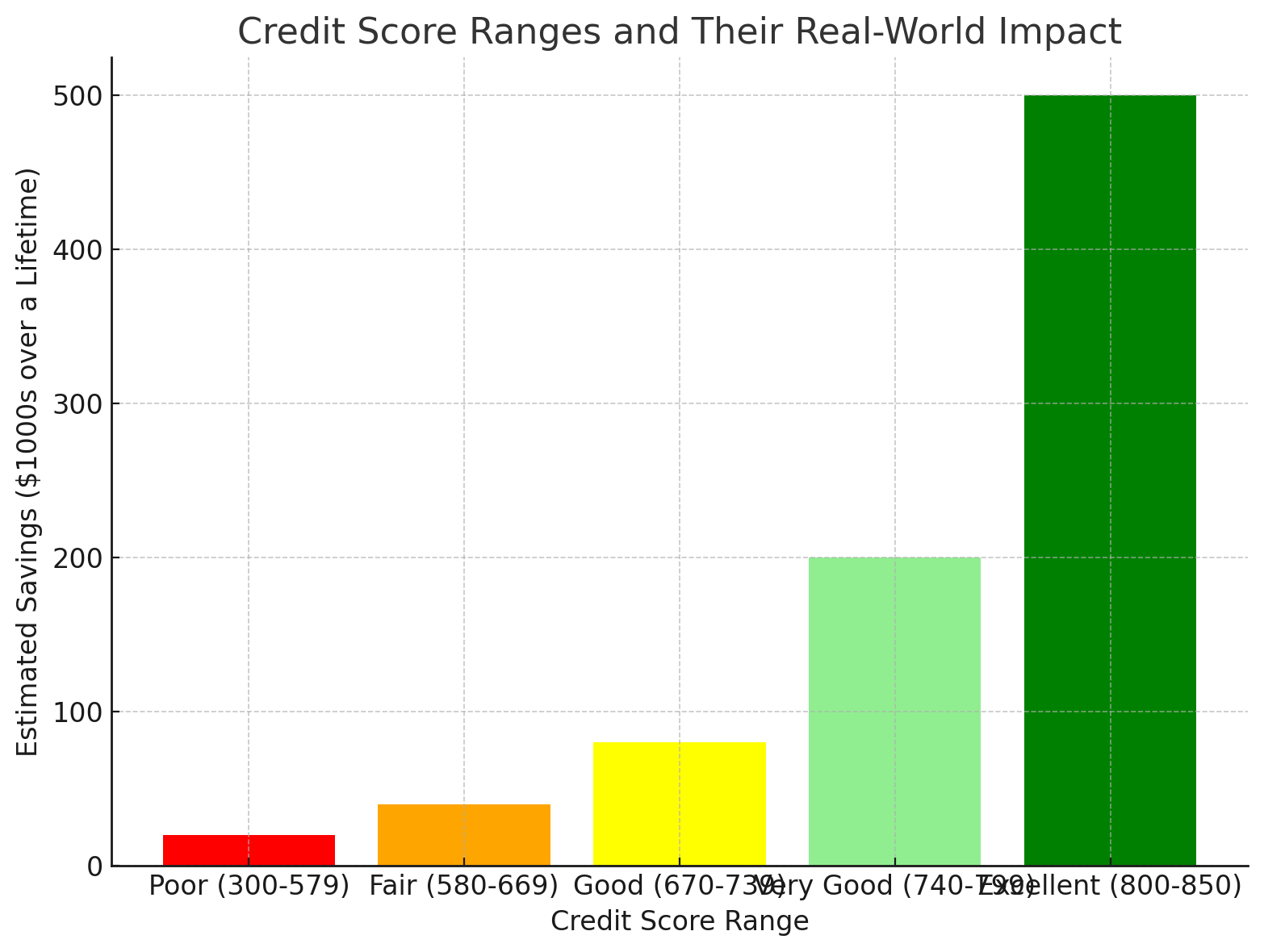

Average college student credit score: 630 (that's like getting a D+ in financial adulting)

The "good" score range: 670-739

Elite tier scores: 740+ (flex material right here)

The Credit Card Chronicles: A Cautionary Tale

I thought getting my first credit card would be the key to financial freedom. I could finally buy the things I wanted without waiting for payday. But after just two months, I’d maxed it out on late-night takeout, concert tickets, and a pair of shoes I wore exactly once. The bill came due, and I realized I had no clue how I’d pay it off.

Therefore, I had to face reality and create a plan. I started tracking every dollar I spent, setting aside a chunk of my paycheck for payments, and learning how to keep my credit utilization below 30%. That one mistake taught me more about money than any class ever did—and it’s the reason my credit score is now flex-worthy instead of a financial red flag.

The Real Tea About Credit Scores

Let's break this down simpler than your ex's personality:

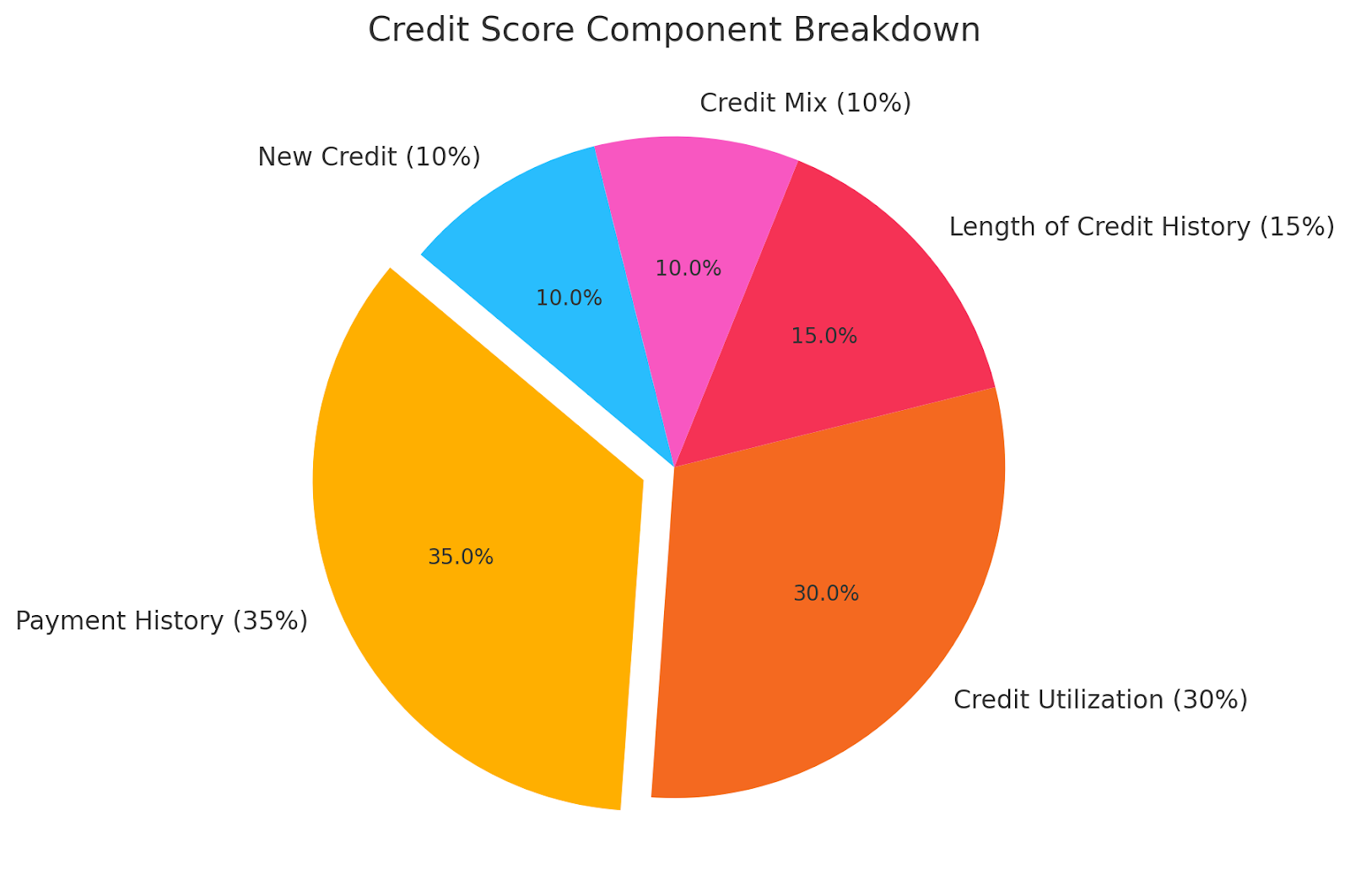

What Actually Makes Up Your Score:

35% Payment History: Like your Snapchat streak, don't break it

30% Credit Utilization: Keep it lower than your dating standards

15% Length of Credit History: The longer, the better (that's what she said)

10% Credit Mix: Variety is the spice of life

10% New Credit: Don't be too eager, playing hard to get works here

The Hard Facts:

Late payments stay on your report longer than that embarrassing photo from freshman orientation (7 years!)

Opening too many credit cards at once is like texting multiple people "you're the only one" - it's gonna backfire

Your credit score can affect:

Getting approved for apartments (no more "my parents will cosign")

Car loan interest rates (that dream car might cost an extra arm and leg)

Future job prospects (yes, some employers actually check this)

Quick Reality Check:

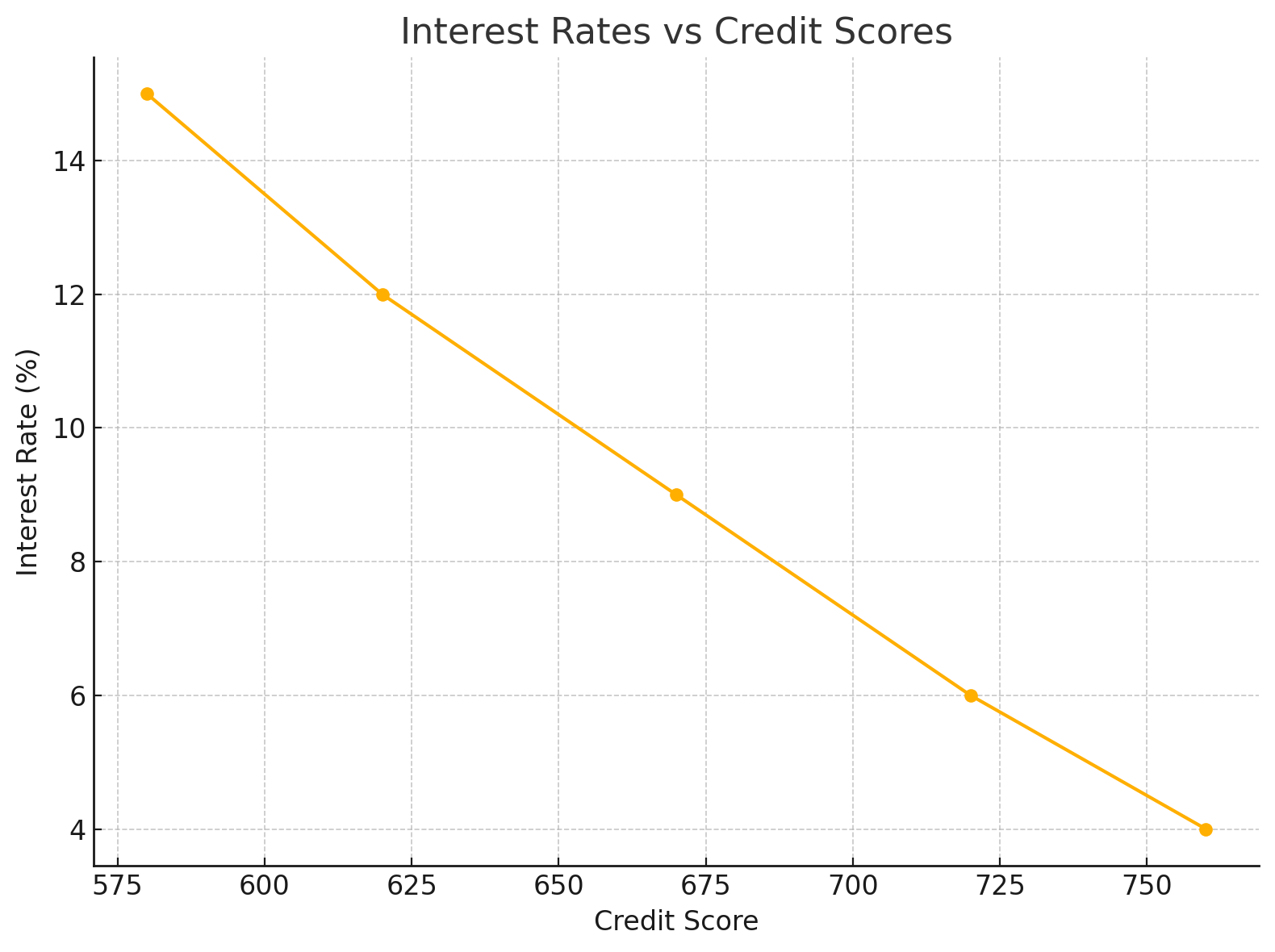

A good credit score isn't just about flexing – it's about saving real money. Example: On a $20,000 car loan:

Bad credit (580): 15% APR = $358/month

Good credit (720): 5% APR = $283/month That's $75 more per month you could be spending on literally anything else.

The truth? Your credit score is basically your financial body count – everyone says it shouldn't matter, but let's be real, it does.

Level Up Your Credit Score: The Strategy Guide

Remember how we said your credit score is like your financial body count? Well, it's time to make it more impressive than your actual one. Let's dive into the forbidden knowledge of credit score improvement that they don't teach in those required financial literacy seminars.

The Checklist:

1. Start Your Credit Journey (Without the Walk of Shame)

Secure that first credit card

Student cards are like using training wheels - slightly embarrassing but necessary

Pro tip: Most banks offer student cards with lower requirements than your dating standards

Start with a secured card if regular cards reject you faster than your Tinder

Discover it® Student Chrome is clutch - they won't judge your non-existent credit history

Look for cards with no annual fee (because you're already paying enough for those textbooks you'll never open)

2. The Payment Strategy (More Important Than Your Study Strategy)

Set up autopay like you set up dating app notifications - immediately and without hesitation

Pay more than the minimum (unlike your effort in group projects)

Keep your credit utilization lower than your GPA goals (under 30%) eg: If your credit card limit is $1,000, never carry a balance above $300. Aim for $100–$200 to maximize your score boost

The "Trust Me, I Learned This the Hard Way" Advanced Tactics

Credit Building Hacks That Actually Work:

Become an Authorized User

Basically, piggyback on your parents' good credit like you do their Netflix account

Just make sure they have good credit (unlike your taste in romantic partners)

Get a Credit Builder Loan

It's like a financial training montage

You're literally paying to build credit (still cheaper than your textbooks)

Use Experian Boost

Get credit for paying your streaming services

Finally, your unhealthy binge-watching habits pay off

The Ultimate Credit Score Cheat Sheet

🟢 DO:

Pay everything on time (treat due dates like delivery pizza - never late)

Keep old accounts open (unlike your toxic relationships)

Monitor your credit report (more regularly than your ex's social media)

🔴 DON'T:

Max out cards (this isn't a game of Pokemon - you don't have to catch all the debt)

Apply for every credit card offer (they're like dating apps - be selective)

Close old accounts (they're like your weird childhood stories - part of your history)

The Final Boss: Long-term Strategy 🎯

Think of your credit score like your GPA for life - except this one actually matters after graduation. A good score (700+) can save you:

$100,000+ on a mortgage

Thousands on car loans

Countless headaches with landlords and employers

The Numbers Don't Lie (Unlike Your Tinder Match)

Let's break down the ROI of good credit:

Average car loan difference: $75/month between good and bad credit

Apartment security deposits: Could save $500-1000

Credit card interest rates: Could vary by 15% or more

That's real money you could be spending on:

75 value menu items per month

15 premium dating app subscriptions

1/4 of a textbook

Your 69-Day Credit Score Challenge

Week 1-2:

Pull your credit report (it's free, unlike your college education)

Dispute any errors (be more aggressive than your DMs)

Set up autopay for EVERYTHING

Week 3-4:

Get your credit utilization under 30%

Apply for a secured or student credit card

Add yourself as an authorized user to a responsible account

Week 5-9:

Make every payment on time

Keep tracking your spending like you track your crush's social media

Don't apply for new credit (play hard to get)

The Long Game (Longer Than Your Student Loan Repayment Plan)

Remember:

Good credit is like good grades - it takes time and consistency

Your credit score can cockblock your dreams faster than your roommate

Building credit is a marathon, not a sprint (unlike your last-minute exam studying)

Action Items (More Important Than Your To-Do List):

✓ Set calendar reminders for payment due dates ✓ Download your bank's app (check it more than your Instagram) ✓ Sign up for credit monitoring (free services exist, unlike your education) ✓ Create a budget (yes, really)

Final Thoughts (TL;DR for Those Who Skip Readings)

Your credit score is like your GPA for life - except this one actually matters after graduation. Start building it now, and future you will be thanking present you more than when you decided not to post that 3 AM story.

Remember: Your credit score might be the only number that matters more than your body count.

Until next time, CoolbyMichael

P.S. If you found this newsletter helpful, share it with your friends who still think credit cards are free money. They need this more than they need another coffee.

Reply